Taking the above example, imagine if the $2 dividend is expected to grow annually by 2%. Congratulations, if you worked along, you have now valued a business using the DCF method. The second approach is by assuming the business is sold at that point. So, given an annual return of 10% on your invested money, to get $10 million by year 3, right now, in your hand today you’d need $7.5 million.

Understanding Terminal Value

This is because if you invested that today with 10% return every year, by year 3 you would have $10 million. You don’t need to worry exactly how the formula itself works too much to perform the method. Investing—you can invest that $10 today, earn, say, 10% interest per year, and in 3 years it will be worth $13.31. If it is, the investment will be profitable and is worth considering.

Understanding Terminal Value and DCF Analysis

Thereafter, we can calculate the present value of the terminal value i.e. we take the value of 980 and multiply it by the year 3 discounting factor (which is 0.8). Finally, the Enterprise Value (943.7) is obtained by adding the present value of free cash flows of years 1, 2, and 3 and the present value of terminal value – representing years 4 and onwards. Projected cash flows must be discounted to their present value (PV) because a dollar received today is worth more than dollar received on a later date (i.e. the fundamental “time value of money” concept). There are two main methods to calculate what the business is worth after the years of your forecast cash flow. We need to know this sum total number so we can add it to the other three years of cash flows, to get the full value of the company’s entire life. The market rate of return on investing money today, tells us how much more that money will be worth in the future because it earns a return.

How Do You Calculate DCF?

- For purposes of simplicity, the mid-year convention is not used, so the cash flows are being discounted as if they are being received at the end of each period.

- Calculate the changes in working capital, add back D&A expense and finance cost as usual.

- In this environment, it’s fair to ask if the discounted cash flow (DCF) analysis and DCF models are still relevant at all.

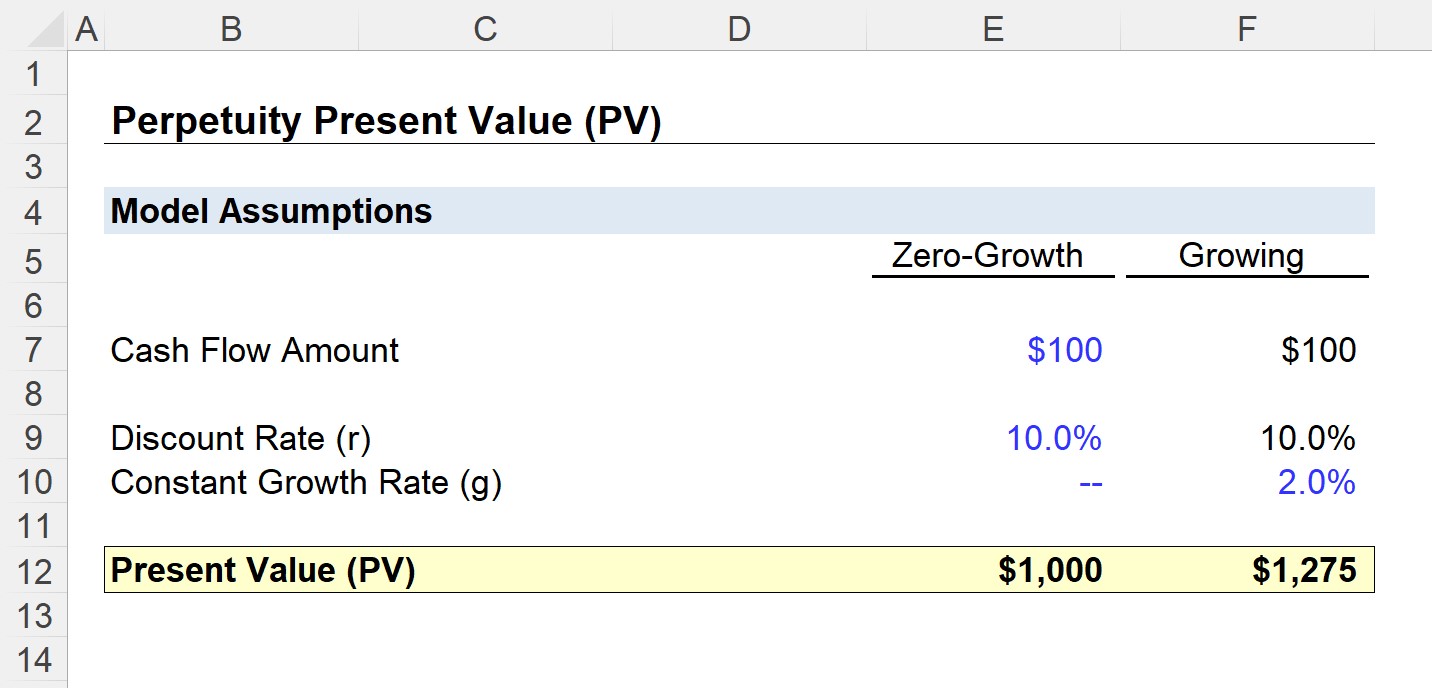

- The DCF method takes the value of the company to be equal to all future cash flows of that business, discounted to a present value by using an appropriate discount rate.

Since the DCF values cash flow available to all providers of capital, EV multiples are generally used rather than equity value multiples. The exit multiple assumption is usually developed based on selected companies’ trading multiples. In certain cases, precedent transaction multiples may be used, depending on the exit contemplated and specific circumstances.

DCF Terminal Value Implied Growth Rate Formula

The two approaches for calculating the terminal value are the Exit Multiple Method and the Perpetuity Growth Method. We use this terminal period to normalize the last year of projected free cash flow, and in turn, we use normalized free cash flow to calculate the terminal value via the Perpetuity Growth Method. All else being equal, a higher % of D&A leads to a higher valuation, because D&A reduces cash taxes paid, thereby increasing cash flow. Using the DCF formula, the calculated discounted cash flows for the project are as follows. As the risk of equity and debt is different(i.e., lower risk to debt holder given more protection), FCFF and FCFE alsorequire different discount rates in the DCF. FCFF is often discounted byweighted average cost of capital (WACC), while FCFE is discounted by cost ofequity.

Terminal Value Formula: Growth in Perpetuity Approach

Alternatively, our team of valuation experts is also available to help you by providing a wide range of services. We charge a reasonable and transparent price and you can have a look at what we can offer here. After deducting the debt value, you now have the equity value of the business (Finally!). Estimate a long term GP margin, EBTI margin, tax rate and net margin.

To calculate UFCF, start with Revenue and subtract COGS, OpEx, and Taxes (which are now different since they’re based on Operating Income). Its annual filing repeatedly cited its total square feet, so we made the total retail square feet the top-line driver and based other numbers on $ per square foot figures. The company’s annual report and investor presentations are the best starting points. Give below are some important limitations of the concept of terminal value of a stock.

Find the per share fair value of the stock using the two proposed terminal value calculation methods. A reasonable estimate of the stable growth rate here is the GDP growth rate of the country. Gordon Growth Method can be applied in mature companies, and the growth rate is relatively stable. An example could be mature companies in the automobile sector, the consumer goods sector, etc.

However, the calculated terminal value (TV) is as of Year 5, while the DCF valuation is based on the value on the present date. Upon dividing the $37mm by the denominator consisting of the discount rate of 10% minus the 2.5%, we get $492mm as the terminal value (TV) in Year 5. Unless there are atypical circumstances such as time constraints or the absence of data surrounding the valuation, the calculation under both methods is normally listed side-by-side. The accuracy of forecasting tends to reduce in reliability the further out the projection model tries to predict operating performance. The second example is in the real-estate sector when an owner purchases a property and then rents it out. The owner is entitled to an infinite stream of cash flow from the renter as long as the property continues to exist (assuming the renter continues to rent).

Terminal value often makes up a large percentage of the total assessed value. The growth in perpetuity approach assigns a constant growth rate to the forecasted cash flows of a company after the explicit forecast period. While the dcf perpetuity formula TV may be calculated using either one of these methods, it is extremely important to cross-check the resulting valuation using the other method. This method is the preferred formula to calculate the firm’s firm’s Terminal Value.