Once the actual increase is computed, it is then adjusted for current year prices and then we can know the total value of ending inventory under dollar-value LIFO. Under Dollar-Value LIFO, COGS tends to be higher because it reflects the most recent, and typically higher, costs of inventory. This increase in COGS reduces the gross profit margin, which in turn affects the net income. While this might seem disadvantageous at first glance, it can be beneficial from a tax perspective. Higher COGS leads to lower taxable income, thereby reducing the company’s tax liability.

FAR CPA Practice Questions: Journal Entries for Treasury Stock Transactions

- In Year 3, there is a decline in the ending inventory unit count, so there is no new layer to calculate.

- An inventory pool is the compilation of similar items in the Dollar Value LIFO method.

- An inventory pool is a grouping of inventory items based on their physical similarities or general category.

- You group DVL pools by year, not unit, so you don’t create new pools when you replace units with different ones.

- Vaia is a globally recognized educational technology company, offering a holistic learning platform designed for students of all ages and educational levels.

This tax deferral can be particularly advantageous in times of inflation, as it allows businesses to retain more cash for operations and investments. Under standard LIFO, you must track your inventory by units, even if you combine similar units into pools. This requires you to track the cost of all purchases and keep records on how you use up your inventory pools through sales. If you adopt the DVL method, you make a physical count of ending inventory and apply the proper DVL cost.

Dollar Value LIFO

(ii) in the case of a cessation of such an election, the 1st taxable year after such election ceases to apply. (B) the adjustment for each such separate pool is based on the change aca frequently asked questions va, affordable care act and you from the preceding taxable year in the component of such index for the major category. This however, was solved with a workaround called LIFO reserve or LIFO Allowance.

Join over 22 million students in learning with our Vaia App

In total, at the end of Year 2, Entwhistle has a base layer cost of $15,000 and a Year 2 layer cost of $24,750, for a total inventory valuation of $39,750. However, it is not clear whether the company actually has more inventory or if it simply paid more and the actual quantity in ending inventory is the same or less than beginning inventory. To determine the correct $value LIFO ending inventory and cost of goods sold, qunatity increases must be separated from price increases.

Create a free account to save this explanation.

In an inflationary environment, it can more closely track the dollar value effect of cost of goods sold (COGS) and the resulting effect on net income than counting the inventory items in terms of units. Like specific goods pooled LIFO approach, Dollar-value LIFO method is also used to alleviate the problems of LIFO liquidation. Under this method, goods are combined into pools and all increases and decreases in a pool are measured in terms of total dollar value. This method requires extensive record-keeping and complex calculations due to fluctuating inventory values. It can lead to significant variances in financial statements, especially in volatile pricing periods, potentially complicating performance assessments for investors.

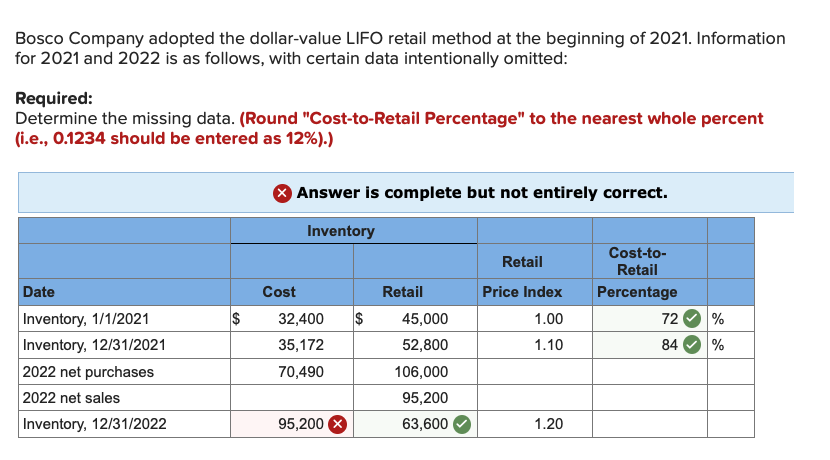

Always consult with an accounting professional or financial advisor when dealing with inventory valuation. The LIFO retail inventory method employs the Last-in, First-out costing method to estimate ending inventory costs. It involves allocating the cost-to-retail ratio to both the beginning inventory and the current period’s layer. In contrast, the dollar-value LIFO retail method considers LIFO principles and adjusts for changes in inventory prices by incorporating fluctuations through the price index. Unlike the prior approach, this process explicitly incorporates variations in inventory prices to determine the estimated cost of ending inventory at annual closing.

The selection of a base year involves some subjectivity, which could affect financial reporting reliability. This method may only suit specific industries where inventory quantity and value changes aren’t closely correlated. Additionally, companies should avoid creating unnecessary inventory pools to prevent increased complexity and costs. By using the latest prices first, cost of goods sold — or COGS — under LIFO is higher, and taxable income is lower, when compared to FIFO.

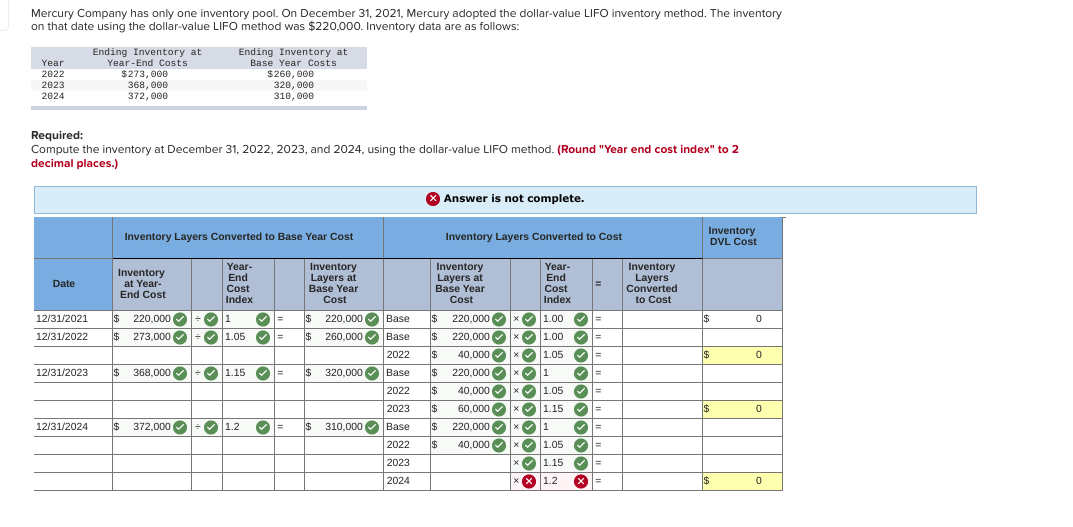

When the adjusted ending inventory exceeds the beginning inventory, it indicates additional purchases, and a new layer is created for the amount of the increase. Choose a base year for the Dollar Value LIFO method, as it’s the year to which you will compare all subsequent years. You will use the prices in this year as a base to interpret changes in the value of the inventory. However, remember, the chosen base year doesn’t influence the dollar value of the inventory; it’s only a point of reference.

Understanding Dollar Value LIFO is crucial for Business Studies because it provides a realistic view of inventory management and cost of goods calculation. Dive headfirst into the world of business studies with a comprehensive look at the Dollar Value LIFO concept. Understanding Dollar Value LIFO, its key components, and its relevance within the field of business is vital for any budding trade professional.

These pools are created to simplify the calculation process by considering a cluster of items, rather than distinct individual items. In Year 2, the incremental amount of cell phone batteries added to stock is 1,500 units. To arrive at the cost of the Year 2 LIFO layer, Entwhistle’s controller multiplies the 1,500 units by the base year cost of $15.00 and again by the 110% index to arrive at a layer cost of $24,750.